Debt is a part of modern financial life for many people, yet it remains one of the most misunderstood aspects of personal finance. From student loans and mortgages to credit card balances and medical bills, most people carry some form of debt in their lifetime. However, the confusion and fear surrounding debt often stem from popular but inaccurate beliefs.

These misconceptions can discourage sound financial decision-making and keep people trapped in poor habits. That’s why it’s essential to explore the top 10 myths about debt you need to stop believing and set the record straight.

In today’s fast-paced economy, being financially literate isn’t optional—it’s essential. Many individuals continue to carry outdated or outright false ideas about debt, which affects everything from their credit score to their ability to secure housing or build wealth. By busting these myths with facts, examples, and current data, you can take control of your finances with confidence and clarity.

Understanding these myths and the realities behind them will empower you to make informed financial decisions and achieve greater stability. In this comprehensive guide, we will break down these widely believed myths and provide evidence-backed insights, useful tips, and clear solutions to avoid them.

Why Understanding Debt Myths Matters

Falling for financial myths can be costly. Misinformation can result in decisions that damage your credit score, increase your interest payments, or prevent you from leveraging useful financial tools. Many people delay important life decisions—like buying a home or starting a business—because of false beliefs rooted in fear and confusion.

Financial Impact of Debt Myths

| Myth Believed | Potential Consequence |

| Closing old credit cards helps credit score | Credit score drops due to reduced credit history and utilization |

| Only making minimum payments is okay | Thousands lost in interest and long repayment time |

| Avoiding credit completely is best | Lack of credit history can prevent loan approvals |

The Role of Financial Literacy in Debt Management

Financial literacy is your best defense against debt myths. Knowing how credit works, how interest accumulates, and how debt impacts your financial health gives you the tools to navigate your obligations confidently. Financially literate individuals are more likely to save, invest, and make choices that reduce long-term debt.

Quick Stats: According to the 2023 NFCC Financial Literacy Survey, only 56% of adults say they have a budget and keep track of their spending, showing a significant gap in fundamental financial knowledge.

Common Beliefs vs. Financial Reality

| Belief | Reality |

| Carrying a credit card balance boosts your credit score | Paying your balance in full is better |

| All debt is bad | Some debt [like mortgages or student loans] can be beneficial |

| Checking your credit score hurts it | Only hard inquiries affect your score |

Top 10 Myths About Debt Debunked

Let’s break down the top 10 myths about debt you need to stop believing and uncover the facts behind each one. Debt myths are not just common—they’re often deeply embedded in the way we think about money, which makes them particularly dangerous. These false beliefs can lead to poor financial decisions, missed opportunities, and increased stress over time. In this section, we go beyond surface-level explanations by offering practical advice, well-researched case studies, and data-backed insights. Each myth is unpacked with user-friendly guidance, empowering you to shift your mindset and adopt healthier financial habits.

Additionally, each section is designed to be scannable and accessible, whether you’re just beginning your financial journey or looking to refine your strategy. We’ll explore not only the truth behind each myth but also how it applies in real-world scenarios. Tables, comparisons, and visual breakdowns will be provided to make the content more actionable. These myths persist because they often contain a kernel of truth, but we’ll separate fact from fiction to guide your next steps. Let’s dive into each myth and uncover what really matters when it comes to managing debt effectively.

Myth 1: All Debt Is Bad

Not all debt is created equal. While high-interest debt like credit cards and payday loans can be harmful, other types of debt—such as mortgages, student loans, or business loans—can help you build wealth and reach long-term goals. This myth oversimplifies a complex issue and may cause people to shy away from beneficial opportunities. The key is understanding the purpose behind the debt and whether it contributes to your future financial well-being. When used strategically, debt can actually open doors, such as investing in education, buying a home, or launching a business. It’s not the debt itself but how it’s managed that determines its impact—wise borrowing backed by a solid repayment plan can be an asset, not a liability.

Types of Debt at a Glance

| Type of Debt | Good or Bad | Notes |

| Mortgage | Good | Builds equity and long-term investment |

| Student Loans | Good | Increases lifetime earning potential |

| Payday Loans | Bad | Extremely high interest rates and traps |

| Auto Loans | Depends | Can be bad if the car is a depreciating asset |

| Credit Cards | Bad if misused | Useful for building credit, harmful if carrying balance |

Example: A study by the Federal Reserve shows that homeowners have 40 times the net worth of renters, highlighting the long-term benefits of mortgage debt.

Myth 2: You Should Always Pay Off the Smallest Debt First

This myth suggests that clearing small debts first is the smartest approach. While the debt snowball method [smallest balance first] can build psychological momentum, the avalanche method [highest interest rate first] saves more money over time. However, the decision between these two methods shouldn’t rely solely on numbers.

Behavioral psychology plays a big role in personal finance—some individuals may benefit more emotionally from small wins, while others prefer the most efficient path financially. It’s also important to consider your monthly budget flexibility and stress tolerance when choosing your debt repayment strategy. What matters most is consistency—whichever method you choose, sticking to it steadily can lead to long-term success.

Debt Repayment Methods Comparison

| Method | Priority | Benefit | Drawback |

| Snowball | Smallest debt first | Motivational wins | More interest paid over time |

| Avalanche | Highest interest first | Saves money | Progress may feel slow |

Case Study: A person with 3 debts [$500 at 18%, $1,000 at 25%, and $5,000 at 12%] using avalanche pays $1,200 less in interest over 3 years compared to snowball. Choosing the right method depends on personal behavior and financial discipline.

Myth 3: Closing Credit Cards Improves Your Credit Score

Many believe that closing a paid-off credit card will boost their credit score. In truth, doing so can lower your score by reducing available credit, which increases your utilization ratio. This is a common mistake for people who want to simplify their finances but end up hurting their credit health. Credit scores heavily weigh the total credit available compared to what you’re using—known as your credit utilization rate.

By closing a card, you reduce that available credit, making it seem like you’re using a larger portion of what remains. Moreover, if the closed card was your oldest, you might also shorten your credit history, which is another key component of your score.

Credit Score Factors Affected by Closing Cards

| Factor | Impact |

| Credit Utilization | Increases [bad] |

| Credit History Length | May decrease |

| Credit Mix | Could reduce variety |

Pro Tip: Keep old credit cards open unless there’s an annual fee or risk of misuse. Credit utilization should be under 30%, ideally under 10%, for a healthy score.

Myth 4: Checking Your Credit Score Hurts It

Checking your own credit score is a soft inquiry and does not hurt your score. Only hard inquiries, such as applying for new credit, cause a temporary drop. Unfortunately, this myth discourages many from monitoring their financial health regularly. Soft inquiries made through tools like Credit Karma or FICO allow consumers to stay informed without any downside.

Regularly checking your credit can help you catch errors early, track your progress, and spot identity theft. It’s a vital habit for anyone looking to manage debt or improve their credit score over time.

Comparison of Credit Inquiries

| Inquiry Type | Triggers | Affects Credit Score? |

| Soft | Personal checks, background checks | No |

| Hard | Loan/credit applications | Yes [temporary drop] |

Insight: Regularly monitoring your score helps you catch errors and track progress. Services like Credit Karma or Experian offer free soft-inquiry checks.

Myth 5: You Only Have Debt If You Owe a Bank

Debt is not exclusive to loans or bank-issued credit cards. Many people carry other financial obligations that qualify as debt. Overlooking these responsibilities can lead to an incomplete picture of your financial health. From unpaid medical bills to overdue utility payments, these lesser-known debts still carry the potential to hurt your credit score and lead to collections. They may not be labeled as “traditional debt,” but they function the same way in how they impact your overall liability.

Recognizing and addressing all forms of debt—no matter the source—is crucial to staying financially on track.

Non-Bank Debts You May Owe

| Type | Source |

| Medical Bills | Hospitals, clinics |

| Utility Bills | Overdue payments |

| Peer Loans | Friends, family, private lenders |

| Subscription Arrears | Services like phone, internet |

Example: In the U.S., 41% of adults carry medical debt. Ignoring these can lead to collections and severe credit damage, making this one of the top 10 myths about debt you need to stop believing.

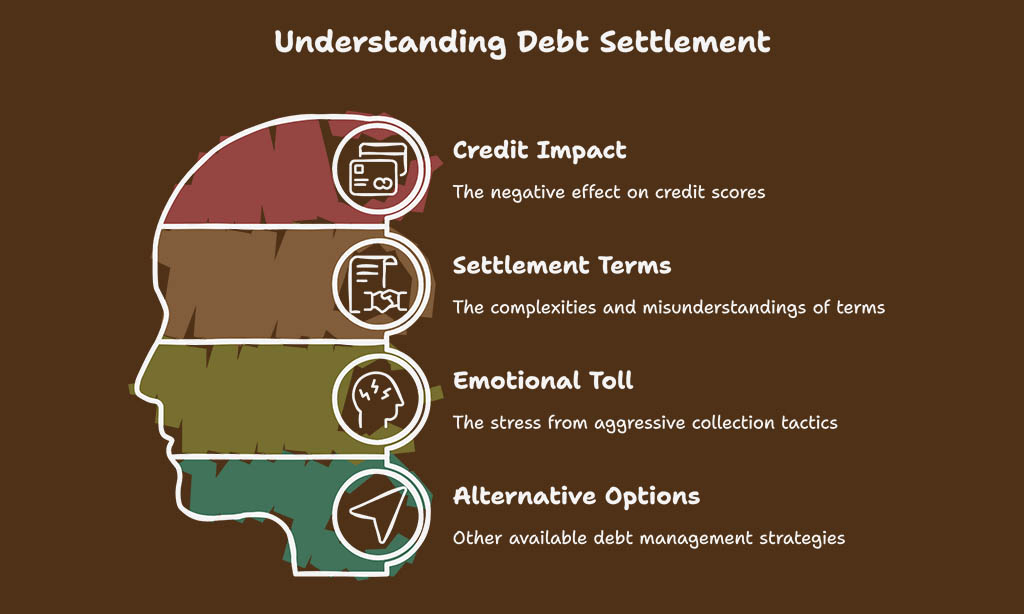

Myth 6: Debt Settlement Is a Quick Fix

While debt settlement companies market themselves as saviors, the reality is often more damaging. Settlement may reduce what you owe, but it severely impacts your credit. Many people are not fully informed about the trade-offs involved—like how settlements can remain on your credit report for up to seven years.

Additionally, some creditors may still pursue the unpaid portion, or the settlement offer may not be honored if terms are misunderstood.

There’s also the emotional toll of navigating aggressive collection tactics while trying to negotiate. Ultimately, it’s important to consult a financial advisor before taking this route, as better options like hardship plans or credit counseling may be available.

Debt Settlement Breakdown

| Pro | Con |

| Lowers balance | Credit score drops significantly |

| Avoids bankruptcy | Debt marked as “settled” not “paid in full” |

| Stops collections | May owe taxes on forgiven amount |

Case Insight: A person who settled $10,000 in debt for $6,000 may still owe taxes on the $4,000 forgiven unless they qualify for insolvency.

Myth 7: Bankruptcy Wipes All Debt Clean

Bankruptcy is not a financial eraser. While it can eliminate many types of unsecured debt, some obligations survive even Chapter 7 filings. For example, recent tax debts, child support, and most student loans are rarely discharged.

Filing for bankruptcy also involves legal costs and court proceedings that can be time-consuming and emotionally taxing. Furthermore, the social stigma and long-term credit consequences may impact your ability to get approved for future loans or even secure housing. Therefore, it’s crucial to understand the full implications and explore all other options before viewing bankruptcy as a solution.

What Bankruptcy Covers and Doesn’t

| Covered Debts | Not Covered |

| Credit card debt | Student loans [mostly] |

| Medical bills | Alimony, child support |

| Personal loans | Recent tax debts |

Insight: Bankruptcy remains on your credit report for up to 10 years. Consider alternatives like credit counseling or debt management plans first.

Myth 8: You Don’t Need a Budget If You’re Managing Debt

A budget is your financial GPS. Without one, you may make progress in one area while sliding backward in another. It gives you visibility into where every dollar goes and ensures you prioritize debt repayments without sacrificing essentials.

Budgeting also helps you identify wasteful spending habits, allowing you to redirect that money toward financial goals. When debt is involved, even small budgeting missteps can compound into larger problems. Having a clear, proactive budget in place gives you control, accountability, and the ability to adjust quickly as your situation evolves.

Top Budgeting Tools & Techniques

| Tool | Platform | Benefit |

| YNAB | Web/App | Zero-based budgeting |

| Mint | Web/App | Automatic expense tracking |

| Envelope Method | Manual | Visual spending control |

Pro Tip: Allocate at least 20% of income to debt repayment. Use budgeting apps to track progress and stay motivated.

Myth 9: Minimum Payments Are Enough

Paying just the minimum keeps you current but allows interest to pile up. This strategy maximizes profit for lenders—not your benefit. Over time, you may find yourself paying two or even three times the original amount borrowed just in interest. This creates a debt trap where progress feels stagnant, and the principal barely decreases.

Additionally, carrying high balances for extended periods may hurt your credit score by keeping your utilization rate high. To avoid this, aim to pay more than the minimum whenever possible—even small extra payments can make a big difference. Developing a consistent repayment habit will accelerate your debt-free journey and boost your financial confidence.

Cost of Minimum Payments

| Balance | Interest Rate | Minimum | Time to Repay | Total Interest |

| $5,000 | 18% | $100 | 7+ years | $4,000+ |

Tip: Even adding $25–$50 more each month can cut years off repayment and save thousands.

Myth 10: Debt Collectors Can’t Do Much

Collectors are limited by law, but they do have rights to pursue unpaid debt within those limits. Understanding the law protects you and gives you the confidence to respond appropriately without being intimidated.

For example, knowing when they can legally contact you—and when they can’t—empowers you to set boundaries and take control of the conversation.

Additionally, staying informed helps you avoid scams or unlawful collection tactics that prey on fear and misinformation. Educating yourself on the Fair Debt Collection Practices Act [FDCPA] can be a game-changer, ensuring you’re not only compliant but also protected. Never hesitate to ask for proof of debt, keep records of all interactions, and seek help if you feel your rights are being violated.

Know Your Rights Under FDCPA

| Legal Actions | Illegal Actions |

| Contacting during legal hours | Threatening arrest |

| Suing for unpaid debt | Harassing calls |

| Reporting to credit bureaus | Lying about consequences |

Pro Tip: Always request a debt validation letter before agreeing to pay. This ensures the collector has legal ownership of the debt.

How to Break Free from Debt Myths and Build Real Financial Health

- Replace debt myths with facts through books and podcasts

- Work with certified financial planners

- Use debt calculators to visualize savings

- Prioritize financial education for long-term change

Financial Tools and Resources

Helpful Resources

| Tool | Purpose |

| Credit Karma | Free credit monitoring |

| NerdWallet | Financial comparisons and calculators |

| NFCC.org | Debt counseling and budgeting support |

Final Thoughts: Stop Believing These Myths About Debt

Believing in misinformation can be as damaging as the debt itself. By understanding the top 10 myths about debt you need to stop believing, you position yourself for smarter decisions and long-term financial wellness.

Debt doesn’t have to be a burden—it can be a tool if managed with knowledge and intent. The key lies in distinguishing helpful debt from harmful obligations and making repayment decisions based on facts rather than fear. By recognizing and unlearning these common myths, you can reduce financial anxiety, avoid costly mistakes, and make informed choices that support your long-term goals.

No matter your financial background or current debt load, there’s always room to grow smarter and stronger. With the right mindset and information, you can take control of your finances, build a strong credit profile, and achieve true financial freedom.